You probably did not get into ministry because you were excited to compare insurance language and think about liability limits. Most church leaders don’t. But at some point, someone has to figure out what risks the church is carrying, whether the current coverage still fits, and what to do next.

This guide is for that moment. Maybe you are buying coverage for the first time. Maybe renewal is coming up fast. Maybe you got a notice from your current carrier and now your week just got more complicated. Wherever you are starting, the goal here is simple: help you understand why church insurance works differently from standard business coverage and what issues your ministry should be thinking through.

At its core, insurance is about sharing risk. Many churches pay into the same pool so that when one ministry gets hit with a big, unexpected loss, there is help there. That is what makes insurance more than a budget item. Yes, it is a form of stewardship. But it is also one of the ways churches help carry each other’s financial burdens when something goes wrong.

What Is Church Insurance, and Why Are You Looking at It Now?

Most churches end up thinking seriously about insurance for one of a few reasons. Renewal is getting close. They are buying coverage for the first time. They got a cancellation or non-renewal notice. Or coverage has already lapsed. Different starting points, same basic job: understand the risk and make wise decisions.

Church insurance is not just business insurance with a church name on it. Ministry creates its own set of exposures: volunteers leading programs, pastors and lay leaders providing counsel, children and youth ministries, mission trips, and community events where just about anyone can walk through the door.

That is why a standard commercial policy can miss the mark. Business coverage is built for business risks. Church life is different. When you try to force one into the shape of the other, the gaps usually do not show up until the timing is terrible.

Why Every Church Needs Insurance

Some leaders still wonder if insurance is really necessary for a small church, especially one that leans heavily on volunteers. Short answer: yes.

Churches can be held legally responsible when someone is hurt, property is damaged, or a ministry decision leads to a claim. Even when your church did nothing wrong, you may still need legal help to respond. Defense costs alone can get expensive fast. Liability insurance is designed to help with covered defense costs and covered damages, subject to the policy’s terms, exclusions, and applicable law.

And the exposures are not hard to imagine. A slip-and-fall can create major medical bills. A data breach can trigger legal, notification, and cleanup costs. An employment dispute lives in its own category of risk and is usually handled very differently from a general liability matter.

If a serious claim goes beyond what your ministry can absorb, the church’s assets may be on the line. That is the real issue here. The question is not whether insurance feels exciting. It is whether your church is protected in a way that actually matches how it operates.

Who You’re Working With: Carriers, Brokers, and Agents

These words get thrown around like they mean the same thing. They do not.

A carrier is the insurance company itself. It underwrites the policy, takes on the risk, and pays covered claims.

An agent or broker helps you navigate the process. Some work with multiple carriers. Some represent one carrier. Either way, the real value is not just getting paperwork submitted. It is helping your church show up well in the underwriting process.

That usually means a good advisor will do a few things well:

- Spot operational weak points early. That might include child safety policies, background checks, incident reporting, document retention, or facility-use procedures.

- Help your church look more organized to underwriting. Clear processes and stronger follow-through matter. Underwriters notice them.

- Frame the account well. If there are past claims, changes in operations, or anything unusual, context matters. A church’s story on paper can affect whether an underwriter sees a risk they want to work with.

Most agents can place a policy. That is not the hard part. The harder part is understanding ministry well enough to ask better questions and surface issues before they become expensive surprises.

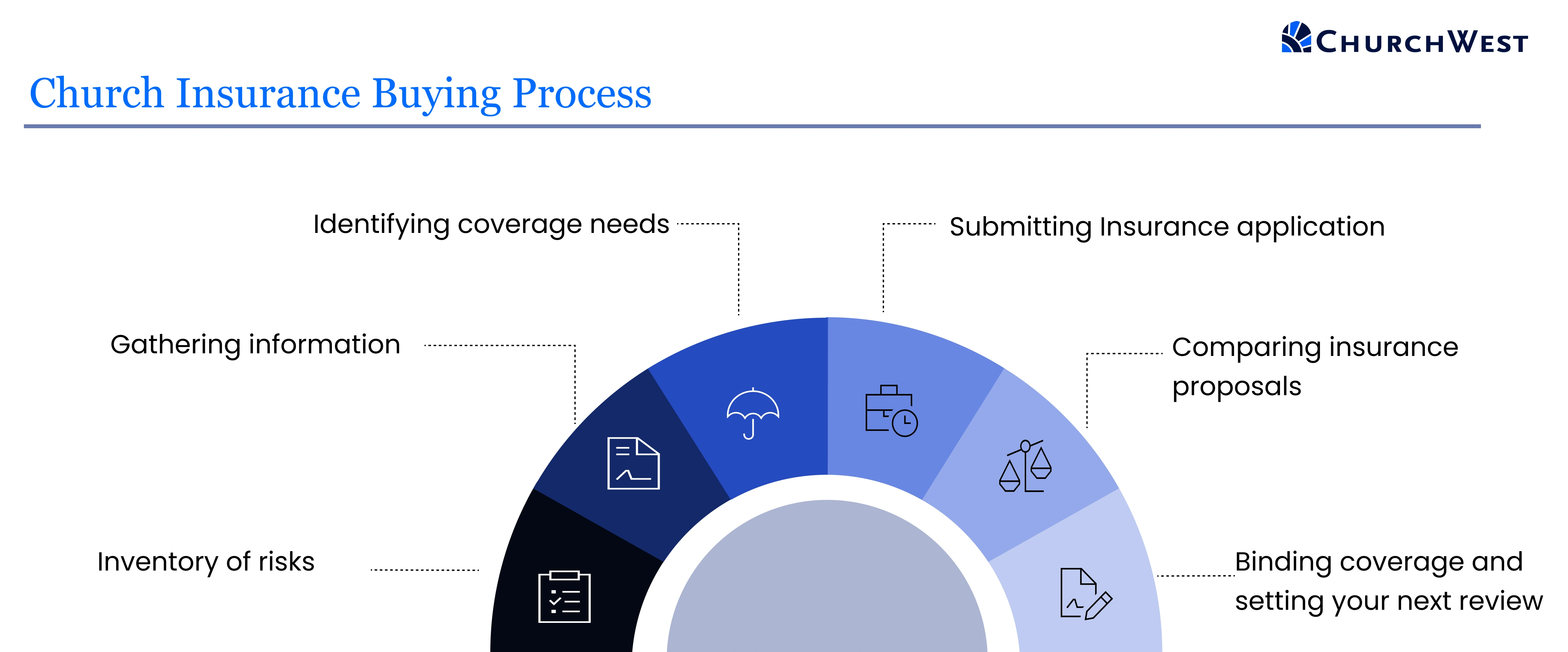

The 6-Step Insurance Buying Process

Buying church insurance can feel like a lot the first time through. The good news is that the process is usually pretty predictable.

Step 1: Inventory your risks. Start with real life, not insurance language. What do you own? What do you operate? Where could something go wrong? Buildings, payroll, kids programs, counseling, vehicles, volunteers, and digital systems all belong in the conversation.

Step 2: Gather your information. Underwriters want specifics. Building details, claims history, payroll, staff count, ministry activities, vehicles, safety practices, and facility-use agreements all help shape the picture.

Step 3: Match risks to coverages. Once you have a clear picture of the ministry, you can start matching exposures to the kinds of coverage that may need to be considered.

Step 4: Work with an agent to submit the application. This is where your information gets turned into an underwriting submission. The goal is not just accuracy. It is clarity. You want underwriting to understand how your church operates and why it is a responsible risk.

Step 5: Compare proposals on coverage, not just price. Two proposals can look similar until you slow down and read what is actually there. Limits matter. Exclusions matter. So do the narrower protections that do not seem urgent until the day they are.

Step 6: Bind coverage and plan ahead for renewal. Before coverage is bound, confirm the entity name, effective dates, locations, and key coverages. Then get your renewal date on the calendar. The more proactive your church is, the better. Underwriters tend to view that as a sign of a better-managed account.

As a rule of thumb, even a smaller church should give the process a little room. Quotes can take a couple of weeks. More complex ministries usually take longer. Starting early makes almost everything easier.

Ready to start the process? A ChurchWest insurance specialist can walk you through it from the first conversation.

The Coverage Your Ministry Actually Needs

Church insurance is not one single thing. It is usually a mix of coverage categories that speak to different kinds of risk. The point here is not to turn you into an underwriter. It is to help you recognize where ministry creates exposures that deserve a closer look.

Property Coverage

Property coverage is about the physical things your church depends on: buildings, contents, equipment, and other assets. And for churches, that can be a long list. Sanctuaries, classrooms, kitchens, computers, sound systems, stained glass, musical instruments, and more can all be part of the conversation. Learn more about church property insurance..

One of the big ministry-specific issues here is building age. Many churches operate in older facilities. Older roofs, older plumbing, and older building systems can make water losses especially painful when they happen. A small leak does not always stay small for long. See how FloLogic helps reduce water damage risk for ministries.

Liability Coverages

Liability coverage is about what happens when a church’s activities are alleged to have caused harm. That can mean bodily injury, property damage, or other kinds of claims. It is a foundational part of a church insurance conversation, but ministry liability is broader than most people expect. Read more about general liability for churches.

Churches should pay especially close attention to exposures involving children and youth programs, counseling, employment decisions, board leadership, and safety or security activities. Those are not edge cases. They are some of the clearest examples of how ministry risk is different from ordinary business risk.

If you want to go deeper on specific liability issues, these guides are a good place to start:

- General liability for churches

- Sexual misconduct liability insurance

- Directors and officers coverage

- Employment practices liability coverage

- Counseling liability coverage

- Safety and security coverage

Workers’ Compensation

In California, workers’ compensation is required for employees, including paid clergy. It helps with medical costs, disability benefits, rehabilitation, death benefits, and employers’ liability protection when a work-related injury happens. There is no carveout here for part-time staff or clergy. Understand workers’ compensation for California churches.

Cyber Liability

Churches now handle more digital information than many leaders realize. Donor records, online giving, email systems, and stored personal data all create exposure. If that information is compromised, the fallout can include notification costs, legal fees, remediation work, and reputational headaches. General liability does not address that kind of risk. Read about cyber liability for churches.

Auto Coverage

Transportation risk is easy to underestimate in ministry. A volunteer driving people to an event may be using a personal vehicle, but the church can still end up pulled into the claim if something goes wrong.

And if your ministry uses 15-passenger vans, the stakes get higher. These vehicles carry serious exposure and deserve extra attention around driver standards, supervision, and operating practices. Learn about auto coverage for ministries.

Mission Travel

Mission travel adds another layer of complexity. Once a team leaves the United States, routine problems can stop being routine. Medical emergencies, travel disruptions, liability questions, and evacuation needs all get harder to manage. If your church sends teams abroad, that should be part of the insurance conversation before the trip leaves the planning stage.

Reinstating Coverage After a Lapse

A lapse means there was a gap between one policy ending and new coverage being put in place. That matters for obvious reasons, but it also matters because underwriters pay attention to it.

When they see a lapse, they usually have questions. What happened? Was it an administrative miss? A budget problem? A leadership transition? What has changed since then? Why is the church in a stronger position now?

Those questions can affect how easy it is to get coverage back in place, what terms are available, and how much explanation the file needs. That is why context matters so much here.

This is one of the moments when a ministry-focused agent can be especially helpful. A good submission does more than admit there was a lapse. It explains what led to it, what has been fixed, and why the church is better organized going forward.

If your church is dealing with a lapse now, the best move is usually to address it directly and quickly. Silence rarely helps. A clear, honest explanation paired with better systems and stronger follow-through can make a real difference.

Why the Cheapest Policy Is Often the Most Expensive

Every church feels budget pressure. That is real. Insurance can look like an easy place to save money, especially when the policy is just sitting there doing nothing visible.

But cheaper coverage is usually cheaper for a reason. Sometimes the core terms are narrower. Sometimes the policy leaves out secondary protections that seem easy to live without until the wrong claim shows up.

That is the trap. A ministry saves a little up front, assumes they are basically covered, and only discovers the gap when the loss is already in motion. At that point, the math changes fast.

The better principle is simple: the right coverage and the right relationship matter more than the lowest premium. That lesson tends to get very clear right after a claim.

Protecting Your Ministry Is an Act of Stewardship

Choosing church insurance is not glamorous work. But it is important work.

It is part of caring for the people in your ministry, protecting the programs they depend on, and preserving the mission your church has spent years building. It is also part of participating in a system where churches help carry each other’s burdens when unexpected losses hit.

The right coverage cannot guarantee a quiet future. What it can do is help your church respond, recover, and keep going when something hard happens.

ChurchWest has protected California ministries for more than 50 years. More than 4,000 churches trust us with their coverage, and our 93%+ client renewal rate reflects what happens when churches find a partner that understands ministry and stays with them through renewals, claims, and growth.

Whether you are buying church insurance for the first time or taking a fresh look at your current program, we are here to help you build something that fits.

Coverage requirements and options vary by state. This guide reflects California insurance regulations and programs available through ChurchWest for California ministries. This content is informational and does not constitute insurance advice. For specific coverage details, consult your policy documents and a qualified insurance professional.

Conclusion

This post was created by the team at ChurchWest to help ministry leaders navigate complex decisions with clarity and care. If you want to explore more resources or talk with our specialists, we are here to help.